Where the 2/20% Venture Capital Structure Comes from

It is really interesting where the 2/20 structure comes from, as it is in effect one of the most impressives pieces of pricing for a strange type of product.

Again, I just want to get this out there. Venture capital, other private equity and alternative asset classes often get paid in the following way: x% of the total money they are investing plus Y% of the returns they generate above some hurdle. Classic case is 2/20.

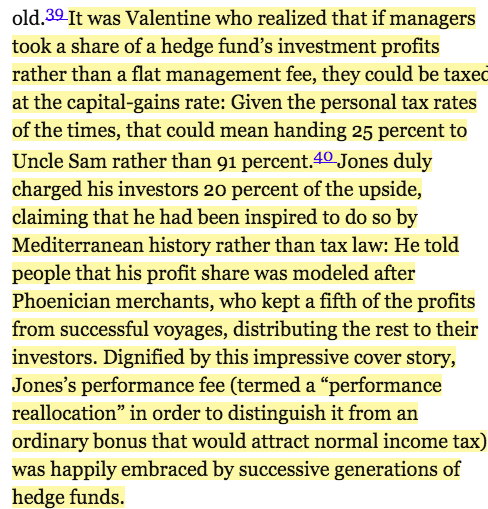

There are a many stories where this comes from: whale hunting, spice trading and other stuff. According to a fascinating book I want to recommend More money than God this is not actually true but what dreamed up by the first Hedge Fund guy. This is fascinating to me because the whaling and other stories are told soo often and apparently it is bullshit.

German Software Stocks - Financial Analysis Intro

As stated previously I will analyse German Software companies. Most financial information is meaningless to me for the purpose of arriving at an attractive price. I can of course compile benchmarks and understand why current coverage, cash cycle theoretically matter but I don’t feel comfortable with it.

What I will do instead is put a value on the whole business then divide that by the number of shares. That will give me the price that I’d be willing to pay for more shares.

But, before I do this I want to share my approach so that I do the same thing for all companies and can improve. This is also written fast and based on common sense. I write we because I own a share of each company.

I will keep this part purely financial, some of the questions serve as preparation for qualitative research or asking the management.

Questions I want answers to:

- Does selling the current products make more cash than it costs to make them?

- Are there more customers for the products with similar acquisition costs in the future?

- Have less people bought our products in the lastly?

- Are we making a lot of investments?

- Have we made a lot of investments in the past?

- How good have the past investments been?

Definition of “Investment” and “Investment” in the context of Software businesses

An “investment” is something that you do today to generate cash in the future. If it does not generate cash it was a bad investment. But, if it does generate cash it is not automatically a good investment. Because it could also not be an investment at all.

Example: If I am in the business of selling balloons on the Oktoberfest, than the thing to put gas into the balloon is not an investment. Yes, it generates cash. Yes, it is re-used when there is gas filled it. But if I buy a new one, I cannot tell my investors that I have “invested” in something. The new gas thing will not generate more revenue at the next Octoberfest, it will just allow me to do any revenue.

Normally, I would expect to find the “investments” in the assets on the balance sheet. Now, in case of software, most likely there will not be an asset on the balance sheet but I expect it to be somewhere on the incoming statement - hidden as labour costs.

Enough theory, let’s start

I feel there has been too much theory from me. I will start and later come back to this article. The questions above still stand.

Share price experiment

Having spend a lot of time on thinking what makes a product profitable, I am not spending more time thinking about what business do. Less on the venture capital side, more on the value investment side. In this article I set the context for a number of analysis that I want to do.

The goal of operating within a company is to generate shareholder value. And, doing that it should not harming the environment, employees or the state. Yes, shareholder value is the focus of the company. The primary institutions to care for the environment, equal opportunity and intergenerational justice are the state and other stakeholders.

Understanding how shareholder value is being generated is therefore essential if you provide labour (as an employee), direct resources within one company (as a manager) or direct resources across multiple companies (as an investor).

I am becoming more interested in understanding how to allocate resources between companies. Plus, I enjoy learning and because of that I will analyse the stocks of software companies listed in Frankfurt.

But before starting that I want to structure my thoughts, otherwise I get lost in information. There are two typical sources of comparisons that I have come across:

- Comparison of data across time

- Comparison of data against other companies

But, I am not really comfortable interpreting this. If I know that a company has more cash on the balance sheet compared to last year - is this good or is this bad? If the company has the highest profit margin compared to “competitors” is this good or bad? Plus, who defines these competitors?

What follows is me trying to think through how I’d value a company before I start doing that with the software companies listed in Frankfurt.

The initial budget

A company starts off with an initial budget. If the company is a consulting operation, this could be the knowledge, reputation and contacts of the person starting it. Example: if you have been a well known professor of accounting it is probably straightforward for you to start an accounting consultancy business. Your prior knowledge, reputation and contacts to potential clients would constitute your initial “budget” that allow you to generate cash through selling your time in the form of consulting. In essence, your time has become a product through your knowledge, reputation and contacts.

The problem is that it is not possible to have an account that has some units of “knowledge, reputation and contacts” on it which you could transfer to a somebody. If that where possible, you could send a couple of units “accounting knowledge and reputation” to somebody and get a % of the money they earned because you gave them the knowledge, reputation and contacts.

Instead of the “accounting knowledge and reputation” account we just have accounts with cash. We want to give this cash to somebody so that they do something with it that results in more cash.

On the one hand, cash is more useful than the account with “accounting knowledge and reputation” on it because we can use it for whatever we want. On the other hand, you have to actually come up with something for that money to do so that it generates more money.

What do I get for my budget

If I had a budget of accounting knowledge, reputation and contacts then I would give that to the person from whom my % would be the biggest amount of cash. That would depend on my negotiation with the person about the relative share of the cut I get, plus my estimation of how much he will make in the future.

Translating that back to an account with money: there are two ways I can get a return on my budget - either I get cash back from a business or the cash stays in the business and as a result, my share of that business gets more valuable. Whether I am able to convert that share of a business into cash is a different question - somebody needs to be willing to buy that share (or the whole thing because 100% of the shares is the whole thing).

That is a serious problem - there are websites that collect other websites where people are trying to sell their businesses! unternehmensnachfolgebörsen.

Value of a share = value of a business / number of shares

Next, I have the problem that one of the two ways of getting something for the budget depends on the opinion of other people - that is the price of my shares. If you have ever sold something it is quite obvious that the price for things is in no way rational in the short term. I will leave this out for now and assume it will take care of itself over the medium term.

Still, the question is how to value the company. If we look back at the example above, where we compared to a person to whom we have given accounting knowledge, reputation and context as the amount of cash that we get back compared to the amount of cash we put in.

Because a company can live forever there are two scenarios to consider. I will use a different example as before for two reasons: 1) I did not plan this article through and 2) I am making a different point with this example then the previous one.

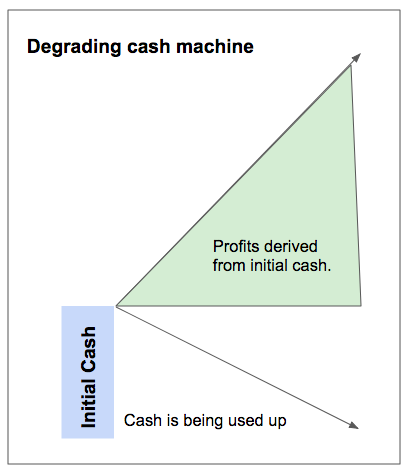

Scenario 1 - Slowly degrading cash machine

In this scenario I put in some cash - say I buy 500 skates boards to rent them in a park. Over time two things happen: 1) cash is being generated and 2) the skateboards break down.

A slowly degrading cash machine

In the graph, “cash is being used up” stands for skateboards break down. This is cash because we have used the cash to buy them and cash generally is a good unit of account. The green thing is the cash generate over the lifetime of the business. It is bigger than the blue block, so that is quite nice. When the all skateboards are broken, nobody cares because they earned more than they cost over time.

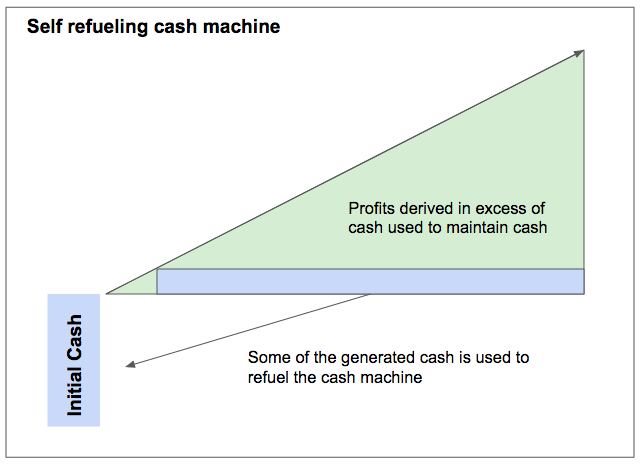

Scenario 2 - Self refueling cash machine

The first scenario makes sense. The second scenario is that a company does not just stop after the initial budget is used up but actually takes a bit of the profits and does something with it to make more cash.

For example, instead of letting the skateboards break down, the company takes that cash and repairs/buys new skateboards. And ideally (!) can rent these skateboards for a higher price or at least the same price. More realistically though, the first skateboards that were rented out where rented out at the highest price and from now on the profits from skateboard renting drops.

The self refueling cash machine

The issues is that the cash can be repleted from three sources: debt, selling of new shares or profits. So it is not as easy as this graph shows but I will learn from application.

Concrete terms for the company analysis

For the below list of companies I want to answer the following questions:

If I buy the company for a given price, will the company generate more cash than that price? (= scenario 1)

If I buy the company for a given price, will the company do something with that cash which enables the company to generate more cash in the future (= scenario 2)

These are the companies that I will put a value on:

ATOSS SOFTWARE AG

COMPUGROUP MED.AG O.N.

FABASOFT AG

FYBER N.V.

GK SOFTWARE SE

INVISION AG

ISRA VISION O.N.

MEVIS MEDICAL SOL.NA O.N.

NEMETSCHEK AG O.N.

NEXUS AG O.N.

PSI SOFTWARE AG

RIB SOFTWARE SE

SAP SE O.N.

SOFTWARE AG O.N.

USU SOFTWARE AG

Analysis: Constellation Software (TSX: CSU) /P1

This is an investing post. I am looking at constellation software (TSX: CSU), a company that has come up multiple times in the past months in podcasts/twitter/blog posts. Writing this as I am educating myself.

This is another type of post. I am writing as I am exploring a company that I have heard more and more about: Constellation Software. Source used are initially the public documents, so statutory filings, the annual letters of the CEO and elements like that.

I am writing here as I read and do not claim to do a deep analysis. The language is how I write, not artificially complex.

Product:

As the company state, this is a holding/investment company. The investment strategy is owning cash generative assets for a long term (as opposed to trading) and use that cash flow to buy other assets. So the cash flow stream does not come from product as such but it comes from the business that then have products. Those I am not looking at those right now, since I am staying at the company level.

Business Model:

In a "normal" business I would look at the unit economics of the products being sold plus the market size for them. Those products generate cash which you can use to make other products that again make more cash or give it back to shareholders.

This company is in the business of buying other companies. That means the company management basically does the product analysis described in the paragraph before. That is the basis of judging the management. Obviously one could form an opinion of the products of the company the management has bought, but this would be more of a qualitative assessment. The equivalent in a "normal" company would be to go on the level of product execution, like a particular advertisement campaign.

Given the above, there are two factors that matter for the business model:

- free cash flow of existing companies

- additional free cash flow generated buy the additional acquisitions

The first bullet point here is basically the running of the existing business, the second part is the "investing element".

Is Michael Porter wrong?

I am trying a new way of writing. Live commenting on the me reading a piece about Michael Porter, the author of competitive advantage and general strategy genius. The foundation for this is the piece "The Gospel According to Michael Porter" from the magazine Institutional Investor.

This is a new way of writing - I am live commenting (minimal editing) the piece The Gospel According to Michael Porter from the Institutional Investor magazine. This is of a lot of interest to me as I have read the key chapter of "Competitive Advantage", sometimes when looking for a strategic way out. It is also interesting to note that reddit has a good thread on this article: https://www.reddit.com/r/SecurityAnalysis/comments/7btb25/the_gospel_according_to_michael_porter/

Here we go.

Porter vs. Graham

The argument is that Porter claims returns are generated through power, whereas Benjamin Graham argues those that going against the consensus leads to outperformance.

Notes:

The take-way is obvious - writing while reading does not work. I do not want to end up re-writing the piece to comment on it. But, I leave up this post anyway, maybe it is still interesting. These comments are quite random, this is not a deep assessment of the piece.

- Power drives the need for market share in pricing

The author argues that the drive for market share is a result of the five forces theory. That is because power is equated with market share. This to me is very interesting since my preference outside extrem growth cases would be to manage on cashflow. Simply because I imagine it very, very difficult to run a large organisation successfully without clear metric. "Growth" is a much less clear metric than free cash flow because it also needs definition of growth in which sector and at what cost. Besides this more managerial point, the author argues that even if growth works, i.e. high market share is achieved this does not translate into profits. Interesting!

- Power as the methodology for anti-trust

It is quite fascinating that business and economic power sometimes does end up in front of a legal system. That is in the case of antitrust law cases. Here without going deeper into the issue which is fascinating, it is ruled that market share in and of itself is not proof of negative influence on the consumer (which would result in excess returns to the company). Read more here: https://www.justice.gov/atr/competition-and-monopoly-single-firm-conduct-under-section-2-sherman-act-chapter-2

- The author

Realising only after the fact that the author is Dan Rasmussen who has an interesting investing strategy by himself. Listen to a good podcast where he explains that here: http://investorfieldguide.com/rasmussen/

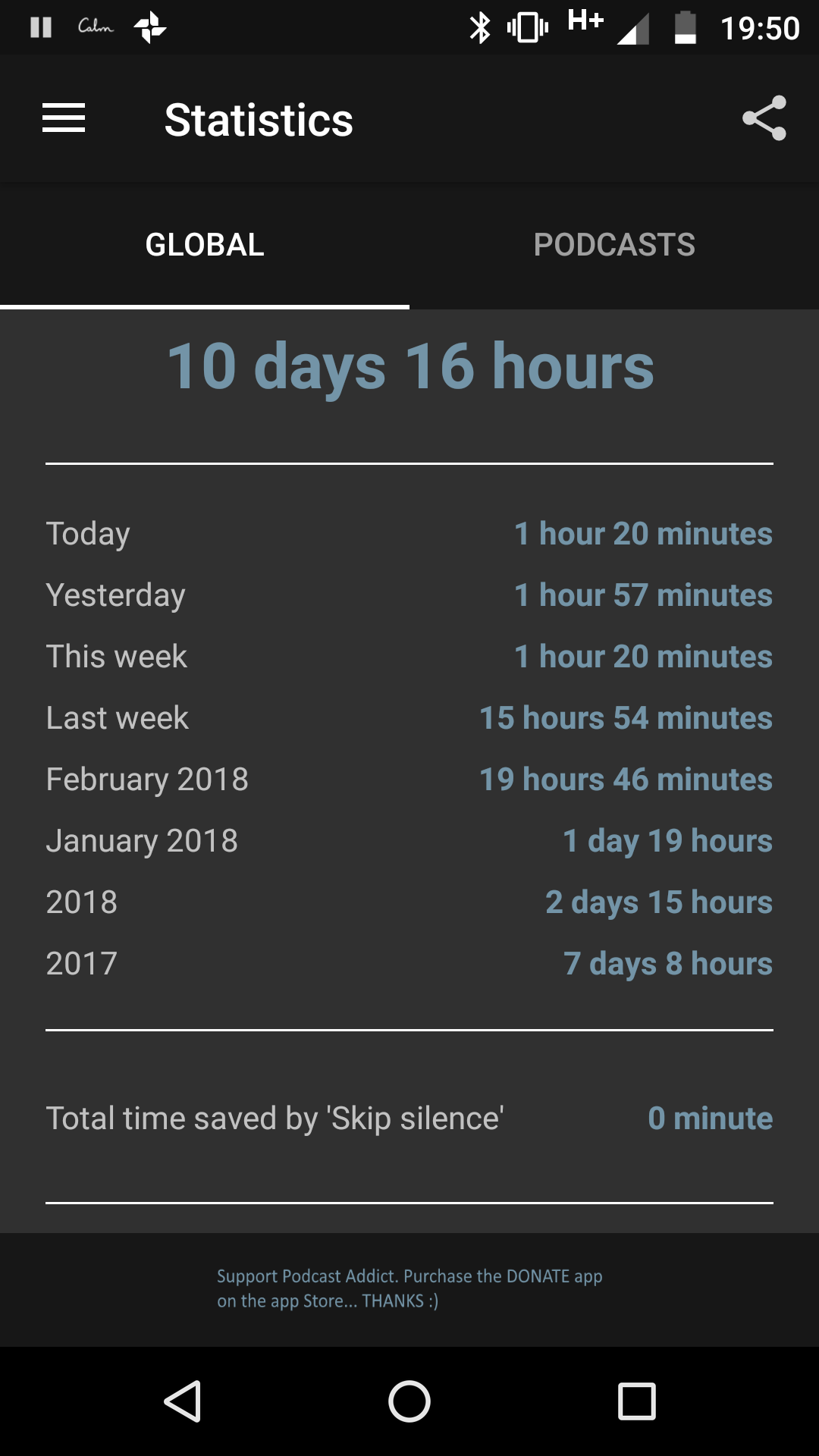

Favourite Podcasts - Product, Investing, Economics, History and Politics - February 2018

A review of which podcast in product management, investing, history and politics I am currently listening to. Plus, personal statistics of podcast consumptions.

Below, I am summing up my current status on podcasting”. As a record for myself (hence the data in the title) and in case anybody is looking for interesting podcasts.

Podcast tools

Subscribe to podcasts on mobile phone: I use Podcast Addict. I chose this about 3 years, paid for it and have my subscription there. Might not be the best tool but does the job for now.

Listen to podcasts on the web: through product hunt or alternatively whatever the website links to that I found googling for a particular topic.

Discovery: most often I listen to podcast when I am interested in a podcast (most recently types of investing other than venture capital). Then I basically google for that topic plus "podcast".

Favourite podcast episodes:

This is just a selection that came to mind while writing, so there are many other excellent episodes.

Current podcast listening statistics

I listen to podcasts usually twice for 30 minutes commuting to work plus when travelling (way to airport, in plane or train) when I am not reading and when I do stuff like preparing washing machines. This results in the following statistics:

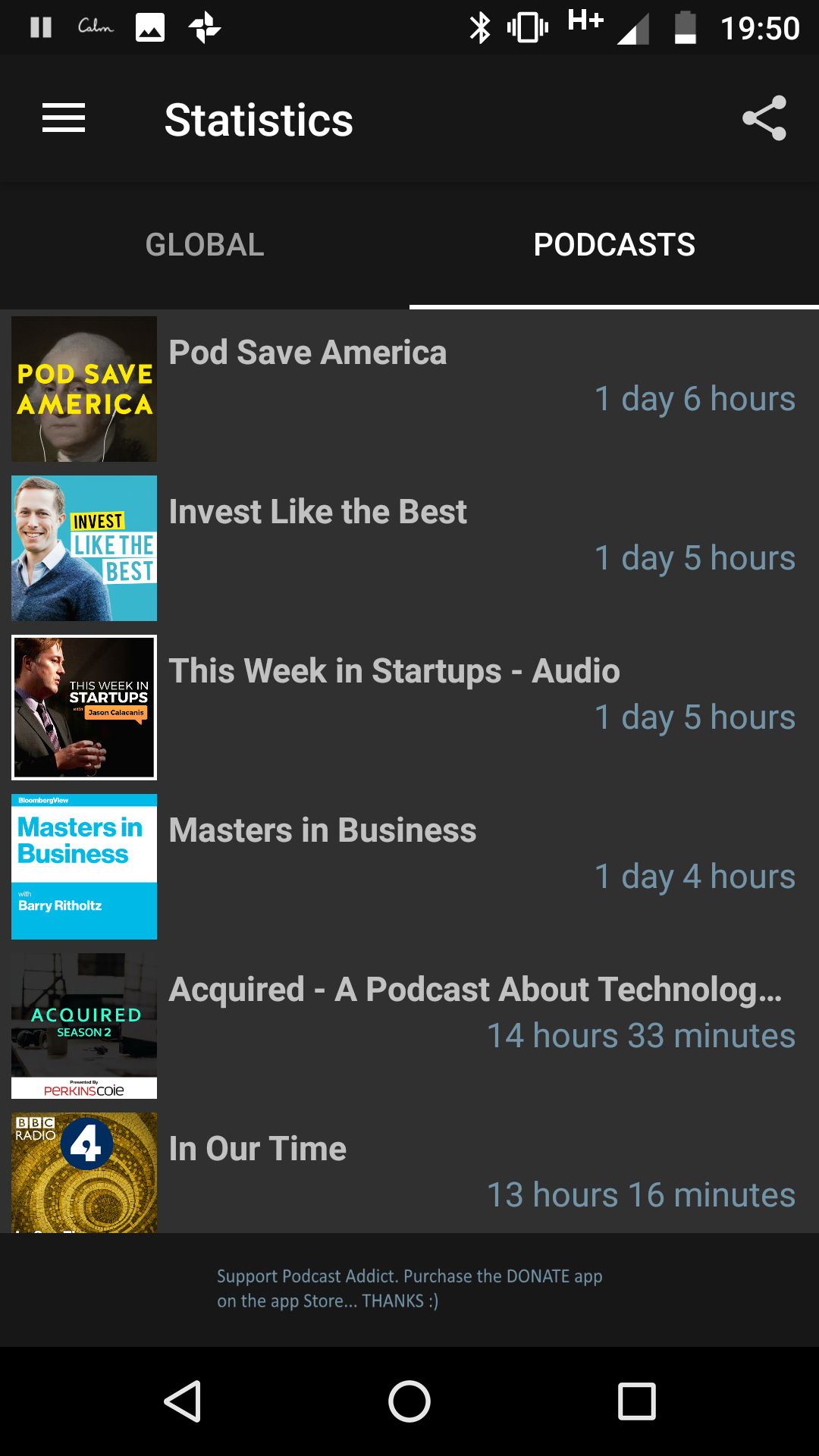

Favourite Podcasts in Economics, History and General

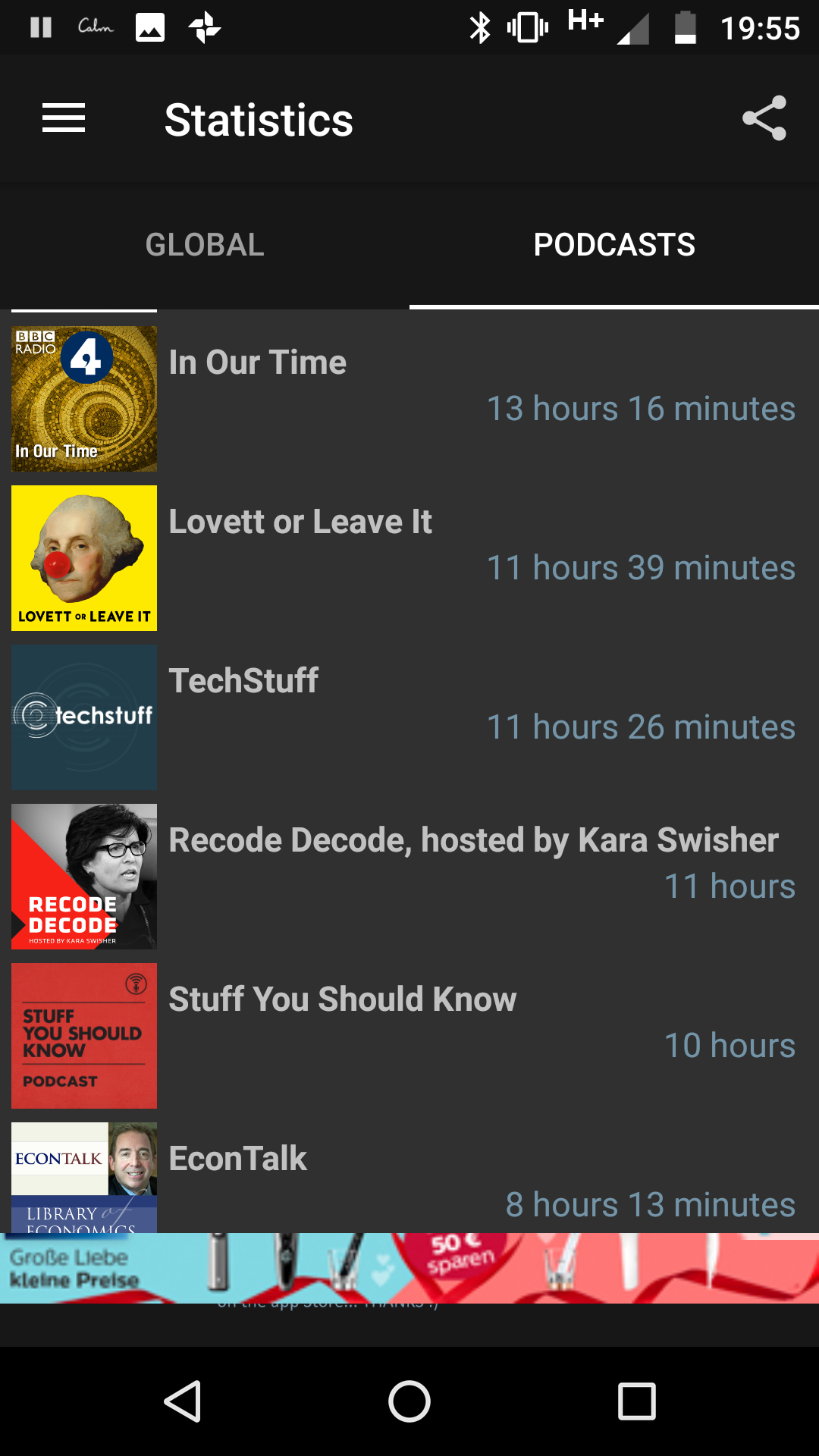

BBC4: In our times podcast - Favourite Episode: P v NP. Extremely fascinating episode. Most of the podcasts are on niche topics but from any area: history, physics, politics, math. Beautiful BBC English.

Econtalk - On of the podcasts I have listened to for the longest time. Most non fiction authors of the type of Books that would be featured in the FT/McKinsey Non Fiction Book of the Year section come through here. Good start before reading the book. Brand name economists like Reinhart (from Reinhart and Rogoff) will show up here as do people like Acemoglu (Why Nations Fail).

Favourite episode: An excellent episode and a very memorable one is Adamati (Bankers' new Clothes) on the cost of equity and how to prevent housing crises. Very understandable for somebody who is not familiar with debt and equity concepts. http://www.econtalk.org/archives/2013/04/admati_on_bank.html

Stuff you should know

No favourite episode. Kind of an an american version of in our times - go through the topics and pick one that is interesting.

Hardcore History - Extremely dense and long history podcasts.

Internet history podcast - If interested in technology or particular companies or technologies from the beginning of the 90ies onwards, this is an extremely interesting podcast. Interesting are the Episodes on Tesla’s founding.

Lovett or Leave it - Entertaining American politics. Sometimes very specific US politics issues. Former speech writer of Obama and Comedian.

The Tim Ferris show - Look at the topics and choose.

Recode/decode - Look at the topics and choose.

Techstuff - Check out the topics and pick what interests you. The episodes on the iPhone are very good but I have listened to nearly all episodes because they interest me,

Favourite Podcasts in Business

Acquired - A history of famous tech M&A transactions and their effect.

Masters in Business - Very listenable on a variety of issues if you are interested in them. I enjoyed the episode with Ed Thorpe because I had been reading about him anyway.

A16z - Future oriented venture capital, the episode on self driving cars could be very interesting.

Invest like the best - Very much enjoy this podcast at the moment. A very fun episode was the a recent one on a variety of different exotic types of investing.

This week in startups - An extremely good podcasts on start ups by Jason Calacanis. The episodes with Chris Sacca, who wanted to be a Spy but then become a venture capitalist are extremely good. As is a more current episode on clean fish.

Meb Farber Podcast - Focussed on investing, I have not listned to many episodes but a current one on leveraging public value equities is quite interesting.

Official SaaStr Podcast - A tactical podcast on the many elements of running a SaaS company.

The IoT Inc Business show - In depth look at a number of IoT specific issues. A good episode compares the different types of protocols. Very useful for current product managers in the space.

Podcasts in product management

This is product management - probably the leader in the space so a bit of a must listen.

Clearly product book club - very good overview of a couple of books you are probably thinking about reading.

How I build this - NPR quality story telling.

There are of course a number of other great podcasts, for example from Deutschlandfunk (German Public Radio), Dittsche (the Hamburg Comedian) and stuff by established media like the economist or the FT that is worth listening to. Not going into detail here because those are somewhat obvious.

Corporate Boards / Initial Thoughts /p1

Recently, two papers have increased my interested in corporate board members: "The Case for Professionell Boards" and "Boards-R-Us: Reconceptualizing Corporate Boards". This posts is my first in a series on board members.

I am starting to write on corporate boards for one reason: I don't understand why investors often are board members. It is not obvious that the skill, incentives and organisations imply that a good investor is a good board member or vice versa.

I also don't understand that if a board is the key high power gremium, how do some people (VCs) and public company CEOs manage to be on multiple boards even though they have a non trivial other job. CEO of a big company or investing fundraising and investing in more companies (VCs). I don't understand this.

The thinking was triggered by a number of conversations and the following research that lead to the The Case for Professional Boards (Pozen, HBS) and Boards-R-Us: Reconceptualizing Corporate Boards (Henderson, Henderson, Chicago School of Law).

As I am approaching this my thinking is not complete. I am writing to complete my thinking. Also, a number of the statements here depend on jurisdiction, I am aware of that.

Duty of a Board Member

Here, I made my first mistake. I believed that the purpose of a board member is to protect the interests of the shareholder he represents. That is wrong. The duties are lined up as follows:

A board member has a fiduciary duty towards all other shareholders

Basically, each board member has the obligation to maximise the outcome against all other shareholders and not just his/her own shareholders. In other words - the duty is against the company (= the sum of all shares), not the CEO, not the other board members, not the shares that the particular board member might own.

That fiduciary responsibility is broken into:

Duty of care

In essence this means that the fiduciary duty can be violated by the board member not being diligent enough. While attempting to act in the best interest (the motivation is right) a board member might be violating the fiduciary duty by not putting in enough work/considering and sourcing the necessary information.

This is in fact an interesting elements with regards to the above questions on the case for professional boards - is it possible to fulfil the duty of care at multiple boards while simultaneously running a company or investing? I am not talking about the intentions, those I presume to be good, just from a capacity point of view.

Duty of loyalty

Obliges board members to put the interest of the company first, their own interests or any other interests second. Obviously, that makes it complex for fund managers that have investors of the funds well.

That is that on board members right now.

Board Member vs Advisory Board Member

The difference is simple: a board member has a duty towards the company (see above), an advisor has the duty to whoever hired him or her.

An advisory board might also be called a "board" but has nothing to do with the corporate board. The obligations are to whoever hired them. Probably, an advisory board is comprised of senior/knowledgeable people expected to give an independent opinion as well.

Still, from a corporate governance (and therefore legal) point of view an advisor, advisory board member or the president of the advisory boards are essentially employees or consultants without any other duty. If they are paid in options, that changes nothing, just makes them an option holder.

That's it for now.